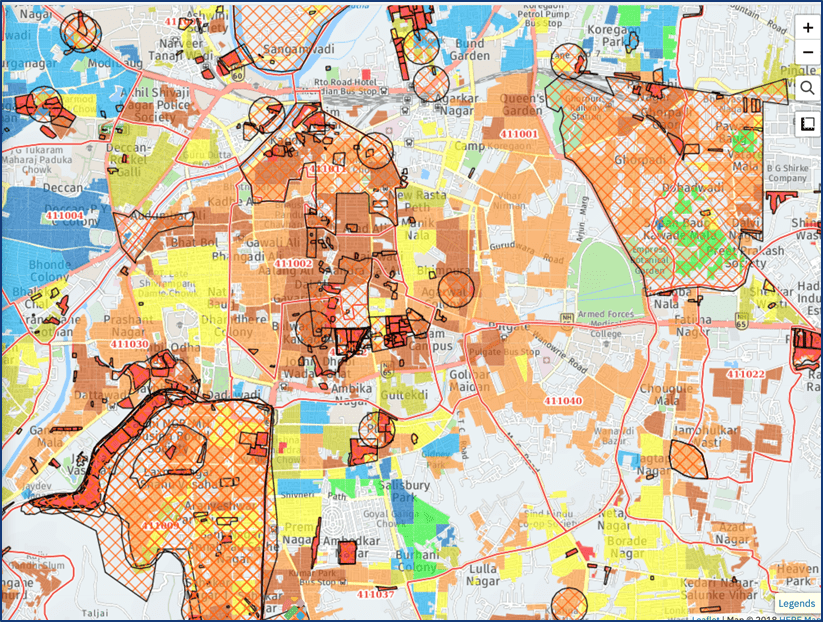

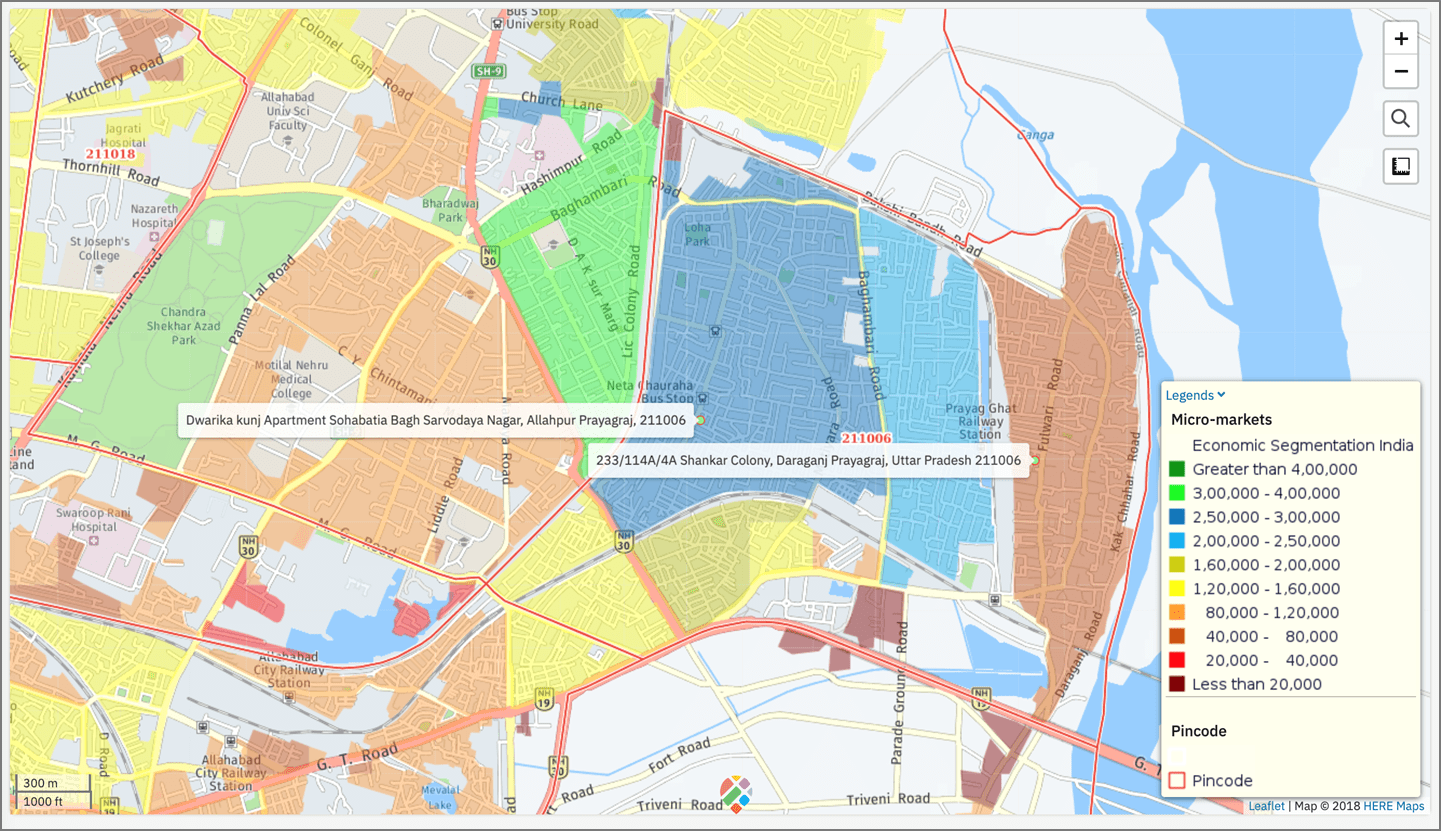

Monthly household-level income score

customer SEC classification

customer

lifestyle affinity segmentation score.

Finding the nearest branch/service station for the customer as per the custom distance criteria implemented custom distance criteria can be set upper regio-type based (Differentiated Urban Classes/Rural) city limits/custom distances for individual product lines.